This week, the total inventory of construction steel continued to decline. The total rebar inventory stood at 5.4782 million mt, down 3.66% WoW. The total wire rod inventory was 1.1222 million mt, down 0.56% WoW. On the supply side, blast furnace steel mills still had profit margins this week, and most construction steel mills maintained normal production rhythms. However, a few steel mills slightly postponed the resumption of production after blast furnace maintenance, while some steel mills continued to suspend their rolling lines. The impact from maintenance on construction steel production was 1.172 million mt this week, up 34,000 mt WoW. EAF steel mills faced poor profitability and mostly maintained production rhythms during off-peak and valley electricity periods, leading to a slight decline in the overall supply of construction steel. On the demand side, construction steel demand was in the transition period between the "off-season and peak season". Downstream procurement was mainly driven by immediate needs, with only a few regions experiencing concentrated procurement due to the accumulation of previous demand orders. Overall, amidst a weak balance between supply and demand, the total inventory of construction steel continued to decline, with the rate of decline slightly expanding.

This week, the total rebar inventory was 5.4782 million mt, down 208,300 mt WoW, a decrease of 3.66% (previous value: -2.43%). Compared to the same period of the previous lunar year, it decreased by 1.7537 million mt, a decrease of 24.25% (previous value: -21.16%).

Table 1: Overview of Rebar Inventory

Data source: SMM

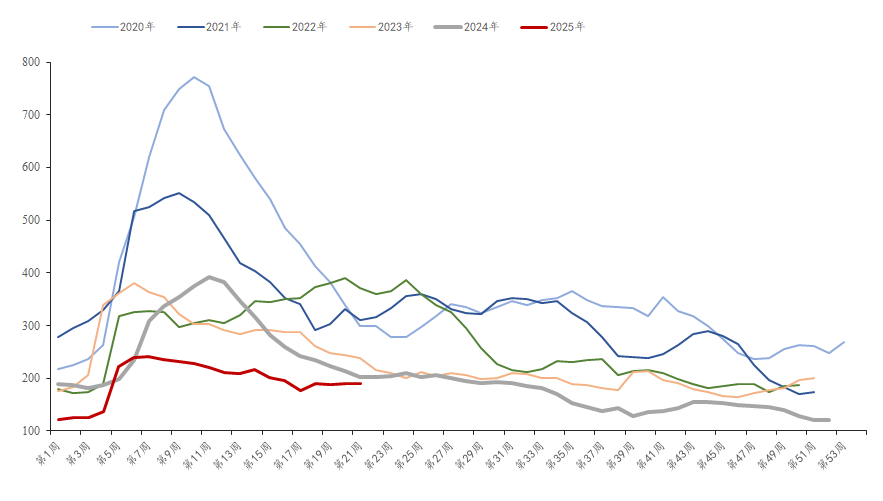

This week, the in-plant inventory of rebar was 1.8982 million mt, down 5,900 mt WoW, a decrease of 0.31% (previous value: 1.52%). Compared to the same period last year, it decreased by 151,700 mt, a YoY decline of 7.40% (previous value: -5.91%). This week, rebar futures prices fell below the 3,000 mark, with market confidence remaining low. Agents mostly operated with low inventory levels, primarily relying on resources dispatched from steel mills. Additionally, some steel mills continued their maintenance and production suspension plans this week, leading to a slight decline in the in-plant inventory of construction steel.

Chart-1: Overview of Rebar Factory Warehouse Inventory Trends from 2020-2025

Data source: SMM

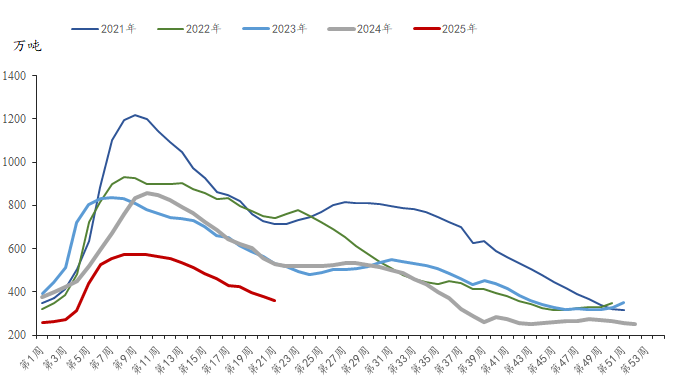

This week, the social inventory of rebar was 2.58 million mt, down 202,400 mt WoW, a decrease of 5.35% (previous value: -4.31%). Compared to the same period last year, it decreased by 1.602 million mt, a YoY decline of 30.92% (previous value: -27.11%). In the early part of this week, construction steel prices were in the doldrums, with market confidence significantly lacking. Traders mostly engaged in selling at low prices. In the latter part of the week, rebar futures fluctuated upward, and market sentiment improved somewhat. The accumulated demand from the early part of the week was released in a concentrated manner. Meanwhile, downstream enterprises began stockpiling in advance of the holiday, leading to a continuous decline in social inventory.

Chart-2: Overview of Rebar Social Inventory Trends from 2021-2025

Data source: SMM

Looking ahead, on the supply side, the profits of blast furnace and EAF steel mills are currently diverging. Blast furnace steel mills still have room for profitability, making it difficult to reduce their production enthusiasm. However, EAF steel mills, affected by difficulties in steel scrap collection and poor profitability, mostly maintain production rhythms during off-peak and valley electricity periods. There is limited room for an increase in their subsequent operating hours. Overall, the supply pressure for construction steel is not prominent at present. Demand side, considering that downstream construction progress will be affected during the Dragon Boat Festival, the pace of purchasing building materials will slow down. Therefore, it is expected that the decline in total inventory of building materials next week may narrow.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)